Mortgage ‘cliff’ looms for homeowners as fixed-rate loans end

When their fixed rate ends in July 2023, RateCity calculated that they would face an average ‘return’ rate of 5.68%, […]

Investment Treaties Could Cure Russia’s Illegal Seizure of Foreign Assets | Cooley LLP

As Reuters recently reported, Russia is preparing a new law that will allow it to seize local businesses from Western […]

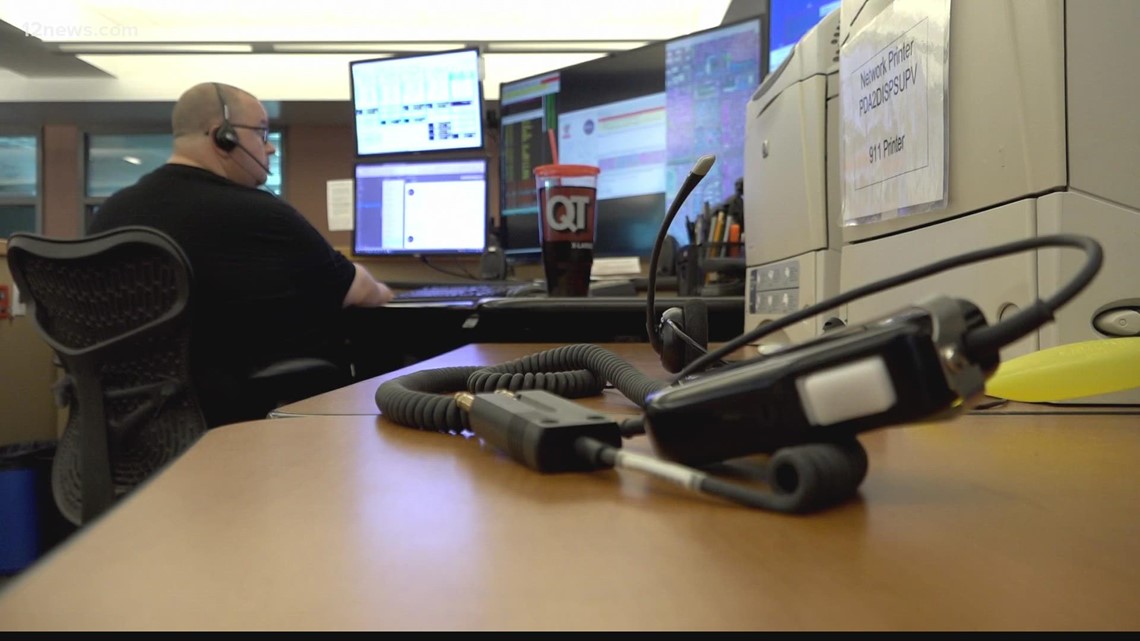

Staffing shortages hurt Phoenix police call response rate

Data from Phoenix PD last year indicates that on average 2 in 10 callers wait longer than 20 seconds. PHOENIX […]

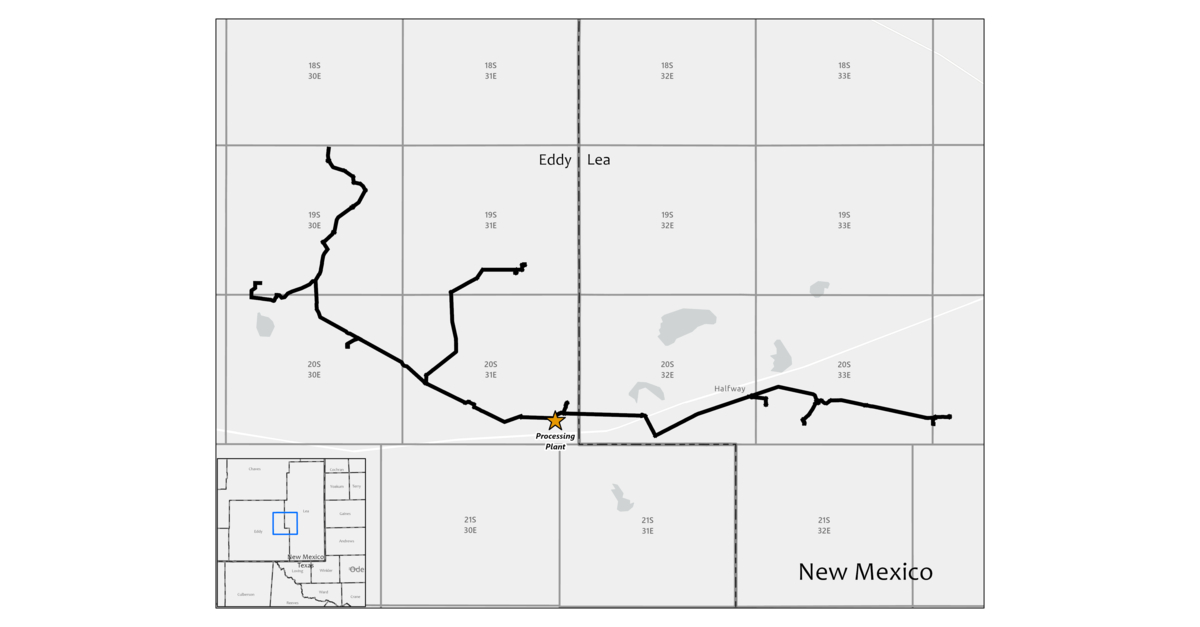

Matador Resources Announces Strategic Acquisition of Midstream Assets in Eddy and Lea Counties, New Mexico

DALLAS–(BUSINESS WIRE)–Matador Resources Company (NYSE: MTDR) (“Matador” or the “Company”) today announced that one of its wholly owned subsidiaries has […]

APC crisis deepens as national working committee orders repeat governorship primaries in Benue council areas

With only a few hours left to submit the list of candidates that have emerged in various primaries organized by […]

Pa. COVID Update: The death rate is increasing slightly. The cases, the hospitalizations continue the descent.

Pennsylvania COVID-19[feminine] the number of cases, which took a noticeable plunge according to last week’s figures from the Pennsylvania Department […]

Tindo Solar and Moula Pay offer working capital to customers

Australia’s only solar panel maker, Tindo Solar, has teamed up with corporate finance expert Moula Pay to allow dealers and […]

100 personal asset plans for a stock split

Over its financial year ended April 30, 2022, Personal Assets generated a return of 7.1% in NAV terms and 8.0% […]

/cloudfront-us-east-2.images.arcpublishing.com/reuters/QBKKFU6ZNBNJ7G4KFURO5MT7XE.jpg)

Covington law firm discloses highest hourly rate of $2,500 in new deal in Ukraine

Covington & Burling offices in Washington, DC REUTERS/Andrew Kelly Join now for FREE unlimited access to Reuters.com Register Summary Law […]

A man hid assets while spending in the casino

ABINGDON – An Abingdon man, who hid bank accounts and other assets from federal bankruptcy court, will serve 12 months […]

Silver Fern Farms signs New Zealand’s largest contract linking working capital and sustainability goals

Provided Silver Fern Farms chief executive Simon Limmer, pictured here launching the company’s carbon-free beef in New York, wants to […]

RBI MPC Meet News live updates: Will RBI go for a 40bp rate hike? What to expect

After May’s surprise off-cycle 40 basis point hike, expectations have narrowed to the size of the hike to rein in […]

Hamilton Lane’s Global Private Assets fund has delivered a 14.7% annualized return since inception in three years since launch

Groundstrokes $2.2 billion in AUM, with an overall Evergreen platform growing to nearly $2.6 billionas company expands investor access to […]

Given Himachal polls, AAP announces new working committee

Building on the recent victory in neighboring Punjab, the Aam Admi Party (AAP) has announced the establishment of a new […]

Deadline Approaches in Texas for SBA Working Capital Loans | KWKT

SACRAMENTO, Calif. (FOX 44) — Many central Texas counties are among the 36 counties eligible to apply for a federal […]

Shelby County gets lower property tax rate for 2023

Shelby County will have a slightly lower property tax rate for fiscal 2023 after commissioners passed a rate of $3.39 […]

BREAKING: Ruling CPA governors, national task force recommend five presidential candidates for primary, advise others to step down

Governors-elect on the platform of the All Progressives Congress (APC) and the party’s National Working Committee have recommended five candidates […]

First batch of non-performing assets will be transferred to bad bank in July: Finance Ministry

The National Asset Reconstruction Company is expected to pick up the first batch of NPAs in July New Delhi: The […]

Count Us In – APC National Working Committee Rejects Lawan as Consensus Presidential Candidate, Emphasizes Position of Northern Governors

The ruling All Progressives Congress National Working Committee said it was not part of endorsing Senate Speaker Ahmad Lawan as […]

CSI will deploy a working capital solution

Corporate Spending Innovations (CSI) will launch a new working capital solution to solve supply chain challenges, according to a Monday, […]

Market expectations for rate hikes too hawkish, says BlackRock

Central banks have pushed markets to be too hawkish on rate hikes, BlackRock Investment Institute said. A recession in the […]

Advisors turn to ETFs as bond mutual funds bleed assets

The first five months of 2022 have been brutal for bond investing, with the Bloomberg Aggregate Bond Index down 9%. […]

UD School of Law invites applications for Student Labor Committee

New Delhi, Jun 06 (PTI) The Faculty of Law, University of Delhi has called for applications for its Student Working […]

Gatekeeper Announces $8 Million in TD Bank Working Capital Facilities to Drive Growth

Abbotsford, BC – TheNewswire – June 62022 – Gatekeeper Systems Inc. (“Gatekeeper” or the “Company”) (TSXV: GSI) (OTC: GKPRF) (FSE: […]

District working committee meeting held, focus on local body surveys

Dar (Madhya Pradesh): The BJP held its district working committee meeting on Monday here at the BJP district office located […]

Jervois Global Increases Working Capital Facility to $150M; Stocks fall 4%

Newswires MT 2022 All the latest from JERVOIS GLOBAL LIMITED […]

Asian stock market mixed, US futures up on concerns over central bank interest rates, crude oil price and yield

Asian stocks traded mixed on Monday as investors gauged the trajectory of central bank monetary policy tightening aimed at stifling […]

Black Money Act order against Anil Ambani: offshore assets Rs 800 crore

ALLEGING the detection of undeclared offshore assets and investments, the Mumbai Unit of the Income Tax Investigation Wing issued a […]

Graham Brady: Chairman of the 1922 committee who may have his own ambitions | 1922 Committee

Sir Graham Brady once joked that the stack of letters calling for a vote of no confidence in the Prime […]

NZD/USD Forex Technical Analysis – Cancel Early Gains on US Rate Hike Fears

The New Zealand dollar closed lower on Friday after hitting its highest level since April 27 amid the possibility that […]

Enhance our tourist assets

Comment marinasb 48 minutes ago – Whether we are monarchists or not, it is right and fitting that we pay […]

PDP appeal committee recommends cancellation and re-run of primary elections in Osun constituency – The Sun Nigeria

Of Lateef Dada, Osogbo The People’s Democratic Party (PDP) Appeals Committee for the State Assembly and Senate Primary Elections in […]

How Detroit Tigers’ Tarik Skubal lowered heart rate; Update from Eduardo Rodriguez

NEW YORK – At the end of the 2021 season, the left-hander of the Detroit Tigers Tarik Skubalnow the team’s […]

Scammers have stolen over $1,000,000,000 in crypto assets since the start of 2021: US Federal Trade Commission

The Federal Trade Commission (FTC) exposes the scope and methods used by crypto fraudsters to amass $1 billion in illicit […]

National working committee meets in Hyderabad in July and focuses on Telangana polls

NNA | Updated: 04 June 2022 16:08 STI New Delhi [India]Jun 4 (ANI): In a bid to bolster its support […]

{kind=link}

Investigational drug adagrasib also shows activity in lung cancer metastases to the brain

According to the results of a study conducted by researchers at the Dana-Farber Cancer Institute. Mutations in the powerful oncogene […]

By 2023, $1 trillion in assets will be gone forever

Over the next six months, the US Federal Reserve will suck more than $1 trillion in liquid assets from the […]

Mortgage of the day, refinancing rate: June 3, 2022

The average 30-year fixed rate fell for the third week in a row, according to Freddie Mac, and now stands […]

Omni and JP Morgan Announce Alliance to Deploy Working Capital Solutions in Latin America

Omni and JP Morgan Announce Alliance to Deploy Working Capital Solutions in Latin America By Edlyn Cardoza June 03, 2022 […]

Refugees can be assets rather than burdens to their new country

5 minutes (1403 words) Lily Download PDF If properly integrated, Ukrainian migrants can bring economic benefits to their […]

The stock-out rate continues to deteriorate, jumping to 73.5%

Shortage of infant formula: a doctor offers advice to parents Infant formula has become scarce on store shelves as the […]

{kind=link}

Connected Assets for Intelligent Operations Are Steadily Gaining Ground – ResearchAndMarkets.com

DUBLIN–(BUSINESS WIRE)–The “Growth opportunities from best practices and new business models in connected assets” report has been added to from […]

Omni and JP Morgan Announce Strategic Alliance to Deploy Working Capital Solutions in Latin America | Your money

BOGOTÁ, Colombia–(BUSINESS WIRE)–June 2, 2022– Omni, the data-driven fintech focused on providing working capital solutions to small and medium enterprises […]

.jpg){kind=link}

Omni and JP Morgan Announce Strategic Alliance to Deploy Working Capital Solutions in Latin America

Bogota – Colombia–(BUSINESS WIRE)–Omni, the data-driven fintech that provides small and medium-sized businesses with working capital solutions in Latin America, […]

PRP inaugurates C’River State working committee ahead of gubernatorial primaries

PRP State Working Committee Members By PATRICK ABANG, Calabar – Edde Iji Edde, a professor of theater and communication arts […]

Comprehensive Report on Working Capital Management Market Trends 2022, Growth Demand, Opportunities and Forecast to 2031

A Working Capital Management report has been released which provides an overview of the global Working Capital Management industry along […]

Tennessee Titans: Robert Woods, a top resource for beginners

NASHVILLE — The list of challenges Robert Woods will face in the weeks and months ahead is long. In a […]

MLB targets broadcaster’s New York assets in $6 million battle

By Caroline Simson (June 1, 2022, 6:55 p.m. EDT) – Major League Baseball has begun targeting assets, including a helicopter, […]

Industry group calls for small independent federal agencies to be given working capital authority

Written by John Hewitt Jones June 1, 2022 | FEDSCOOP The Digital Innovation Alliance has called on lawmakers to extend […]

Should I change banks to benefit from a better interest rate?

The Federal Reserve has signaled that more interest rate hikes are coming this summer. It is worrying if you borrow […]

{kind=link}

BJP state working committee meets historically: Yadav

The two-day BJP State Working Committee ended Monday in Hazaribag at Aranya Vihar Hotel. At this meeting, the state in […]

Boston Asylum Office has second-lowest approval rating in nation – NBC Boston

New England congressional leaders are calling for a federal investigation into the region’s low asylum office approval rate. US Senator […]

{kind=link}

Visa strengthens Fundbox’s working capital platform with digital payments

Visa (NYSE:V), a global leader in digital payments, today announced its partnership with Fundbox, an integrated working capital platform for […]

Spirit Energy Completes $1.1 Billion Sale of Norwegian Oil & Gas Assets

The Statfjord A platform in the North Sea. Credit: Øyvind Hagen / Equinor ASA. Spirit Energy, a subsidiary of Centrica, […]

Bay Area amid another COVID surge, has highest infection rate in California

SAN FRANCISCO (KGO) — The Bay Area is facing another surge in the pandemic and now has the highest COVID-19 […]

India Inc profits rise in Q4 FY22, but working capital is the problem

Macro image looks encouraging on sales If you were to take the 2,900 companies that have announced their results so […]

Lakers don’t want to use their assets to trade Russell Westbrook

NBA Analytics Network The Los Angeles Lakers made their first big move of the NBA offseason, announcing that Milwaukee Bucks […]

Zinc8 Energy Solutions Inc ends the first quarter with a working capital balance of $7.5 million

Zinc8 Energy Solutions (CSE:ZAIR) Inc said it filed its financial results for the first quarter ending March 31, 2022, noting […]

What about the CBN benchmark rate hike, By Uddin Ifeanyi

Central Bank of Nigeria (CBN) A more effective monetary policy regime (there is less talk of a transparent monetary policy […]

The accounting period of foreign assets

It is mandatory for anyone qualifying as a “resident and ordinarily resident” of India to file an income tax return […]

Our View: US Road Fatality Rate Still Rising in New Jersey | Latest titles

This month’s annual road toll report from the National Highway Traffic Safety Administration contained the dismal data the public has […]

What Led To The Crash Of Crypto Assets UST, Luna And Its Impact On Indian Investors

“As such, we refute the popular narrative of an ‘attacker’ or ‘hacker’ working to destabilize the UST. Rather, the UST […]

Yogi to inaugurate BJP state working committee meeting, several UP union ministers likely to attend

Chief Minister Yogi Adityanath will inaugurate the Bharatiya Janata Party State Working Committee meeting in Lucknow on Sunday. The party […]

Mortgage rates today, May 28 and rate predictions for next week

Today’s Mortgage and Refinance Rates Average mortgage rates barely budged yesterday. However, overall, the week was favorable for these rates. […]

UP BJP may have a new president today, BJP working committee meeting”

Lucknow: After recording a massive victory in the Uttar Pradesh parliamentary elections, there has been suspense over the new BJP […]

Genius Assets is launching the GeniuX Era competition with

Arad, Romania, May 27, 2022 (GLOBE NEWSWIRE) — Genius assets, a one-stop solution for all investment problems, has launched the […]

Officials are ready to dip into working capital to limit water and garbage costs in villages

North Sumter County Utility District Board signals it will dip into working capital in the coming financial year rather than […]

/cloudfront-us-east-2.images.arcpublishing.com/reuters/OJQO5ZXM3FOTLPHXQKBRWPSAMM.jpg)

Cooling US inflation argues for slower Fed rate hikes in September

May 27 (Reuters) – Evidence that U.S. inflation is cooling will not move Federal Reserve policymakers from the half-point interest […]

/cloudfront-us-east-2.images.arcpublishing.com/reuters/YOPBVOQRH5PKLDXMDQFDYX7CIY.jpg)

India Oil cos $125.5m dividend from oil assets stranded in Russia

NEW DELHI, May 27 (Reuters) – Indian companies with stakes in two Russian assets are unable to repatriate 8 billion […]

/cloudfront-us-east-2.images.arcpublishing.com/reuters/VJBM6FIP6ZNKZCF6TQAUFMEZ2M.jpg)

Dollar set to see biggest weekly drop in nearly 4 months as rate bets cool

U.S. dollar bills are seen in front of a stock chart in this November 7, 2016 illustration. REUTERS/Dado Ruvic/Illustration/File Photo […]

Japan remains top creditor as net foreign assets rise

TOKYO, May 27 (Reuters) – Japan’s net foreign assets hit a record high in 2021, maintaining its position as the […]

Traders cut expectations for Fed rate hikes in 2022 as economy contracts more than expected in first quarter

Fed funds futures traders are backtracking on their outlook for further rate hikes as revised data released Thursday shows the […]

Vanguard Sees Half of Actively Managed Assets Aligned to Net Zero by 2030

Says 17% of actively managed assets are currently aligned Expects this figure to reach at least 50% by 2030 $5 […]

Maryland insurers in individual market seek 11.2% rate hike

“It is clear from our ongoing monitoring of industry experience that 2021 claims have been heavily impacted by COVID-19,” says […]

The Fed sees asset prices as high and expects to raise rates further

WASHINGTON, DC – OCTOBER 04: Chairman of the Federal Reserve Board Jerome Powell attends an event at the … [+] […]

Paisabazaar closes its largest working capital loan of Rs. 4.5 billion

NNA | Update: May 25, 2022 5:40 p.m. STI Gurgaon (Haryana) [India], May 25 (ANI/NewsView): Paisabazaar, India’s largest digital marketplace […]

The market for cash and working capital management services could see a big movement: AGS Transact Technologies, CapActix Business Solutions, Grant Thornton

This press release was originally distributed by SBWire New Jersey, USA – (SBWIRE) – 05/25/2022 – Latest industrial growth study […]

Easy access to working capital for MSMEs

MSMEs have been leading the country’s growth for the longest time, and throughout the pandemic they have shown that they […]

Kalispell examines the increase in the rate of waste

Responding to inflationary pressures while aiming to fully serve the city, Kalispell is considering a potential increase in its garbage […]

Fundbox builds a working capital solution on the Stripe platform

SAN FRANCISCO, May 24, 2022 (GLOBE NEWSWIRE) — Box today announced that its working capital platform is now integrated with […]