/cloudfront-us-east-2.images.arcpublishing.com/reuters/EAZPCMIOMBOMDF2KAGI3OAZCSA.jpg)

Peak balance sheet: Fed assets fall to level of 5 weeks ago. End of QE, end of an era

The markets have already started saying goodbye to this easy money.

By Wolf Richter for WOLF STREET.

The Fed’s weekly balance sheet total assets as of April 20, released this afternoon, fell to $8.955 billion, about the same as March 16 and below March 23 and March 23 levels. April 13. Beyond the week-over-week highs and lows caused by the peculiarities of Mortgage Backed Securities (MBS), which we’ll get to in a moment, the balance sheet has flattened. Balance sheet growth is complete. EQ is complete. This part of the wonderful show is over.

Since March 2020 when this whole money printing orgy started, the Fed has increased its assets by $4.65 trillion, a staggering amount of QE in just two years.

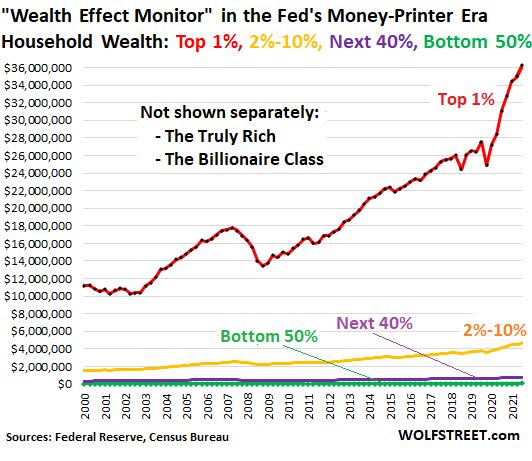

QE was designed to suppress long-term Treasury yields, mortgage rates, long-term interest rates of all kinds, and to inflate asset prices. This has thus created the largest wealth disparity on record, documented by my Wealth Disparity Monitor, based on the Fed’s own data.

But then runaway inflation got in the way. And the Fed finally began to “reduce” its asset purchases in mid-November. Tapering means the Fed bought fewer Treasuries and MBS than it did before tapering, when it was increasing its assets by about $120 billion a month. After the reduction began, this monthly increase began to decline. Now the balance sheet is no longer growing, tapering is over and QE is over.

Now the markets have started saying goodbye to that easy money. The bond market has been hammered since last year. The stock market has been hammered since January of this year and many stocks have imploded.

The Fed also unwound and rolled back to zero many of its emergency measures it launched in the spring of 2020, including its repos, which it ended in mid-2020, and its corporate bonds and ETFs. bonds, of which she never bought much. to start. We’ll come back to that in a moment.

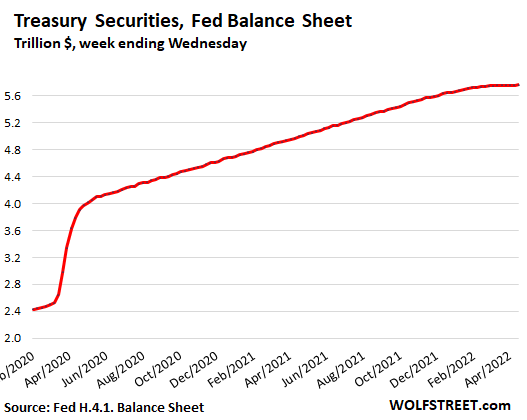

Treasuries are flat at $5.76 trillion.

Since early March 2020, the Fed’s holdings of Treasury securities have ballooned by $3.24 trillion, to a total of $5.76 trillion. The balance has now remained roughly stable for several weeks.

In order to maintain the balance of Treasury securities at the current level, as maturing securities leave the balance sheet, the Fed buys new Treasury securities in the quantities necessary to replace maturing securities.

TIPS fall, accumulated inflation protection rises.

The $5.76 billion in Treasury securities includes Treasury Inflation-Protected Securities (TIPS) and the inflation protection accumulated on those TIPS. The government compensates TIPS holders for CPI inflation by increasing the principal of TIPS. The Fed tracks this amount of “inflation protection” separately from the face value of the TIPS. On his record today:

- TIPS, face value $381 billion, -$7 billion since March 16.

- Accumulated inflation protection on TIPS, $81 billion, +$4 billion since March 16.

The Fed’s sleight of hand with TIPS on market-based inflation expectations.

Since March 2020, proportionately huge Fed purchases have dominated the relatively small TIPS market and pushed TIPS yields into the negative.

TIPS yields are referred to as “real yields” and are a factor in “market-based” inflation expectations (such as the spread from regular Treasury yields) that the Fed has cited in its statements to show that market-based inflation expectations were “well-anchored”, when in fact these “market-based inflation expectations” were the result of TIPS yields that the Fed manipulated lower with its purchases of TIPS.

With its purchases, the Fed pushed the 10-year TIPS yield into negative territory throughout the pandemic. But the Fed has now stopped buying TIPS, and the TIPS balance is down on its balance sheet, and TIPS yields started to rise in January (from -1.1% at year-end) to a just over 0% on April 19, the first time since March 2020 that the 10-year TIPS yield closed in the positive, but for just one day.

Manipulating the yield of TIPS to show that “market-based inflation expectations” were “well entrenched,” despite inflation having already begun to rage, was one of the most smart.

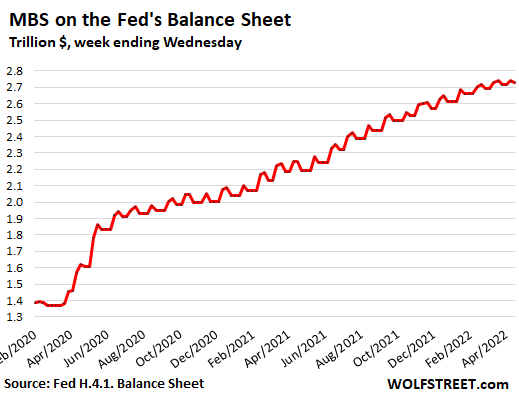

MBS: $2.73 trillion, stable with March 16.

The Fed’s holdings of MBS fell to $2.73 trillion on the balance sheet today, and were about flat with the March 16 balance. Since March 2020, the Fed has added $1.36 trillion in MBS.

MBS differ from regular bonds in that holders receive capital payments passed on when the underlying mortgages are paid off after the house is sold or the mortgage is refinanced, or when regular mortgage payments are made. As a principal payment is made, the MBS balance decreases by that amount.

During times of low and falling mortgage rates, such as during the pandemic, mortgage refis are a huge thing, and principal passthrough payments become a torrent, and the balance of each MBS dwindles rapidly.

Conversely, soaring mortgage rates have now largely killed refis, and passed-on principal payments have slowed.

In order to offset these passed-on principal payments, the Fed buys large amounts of MBS in the “to-be-announced” (TBA) market. Before the shrink, it was buying more than $100 million a month to offset principal passthrough payments and increase the balance sheet by $40 billion a month.

Now he buys just enough MBS to meet the estimated amount of passthrough principal payments to keep MBS at its balance sheet level.

But there are two problems with this:

- The unpredictability of principal passthrough payments

- The 1-3 month delay before the Fed’s MBS purchases on the TBA market settle.

Trades on the TBA market take one to three months to settle. The Fed books its transactions after they have been settled. So when the Fed was three months into its cut, that’s when the first tapering MBS purchases started showing up on its balance sheet. This is delayed data. And MBS on the Fed’s balance sheet continued to rise at the pace of purchases two to three months earlier.

Also, the timing of principal passthrough payments and purchase settlement do not match week to week. Thus, the Fed’s MBS balance goes up and down from week to week.

At this time, most deferred settlements of progressive MBS purchases have been accounted for, although there may still be some latecomers. And the MBS balance, despite week-to-week ups and downs, is pretty much flat with March 16:

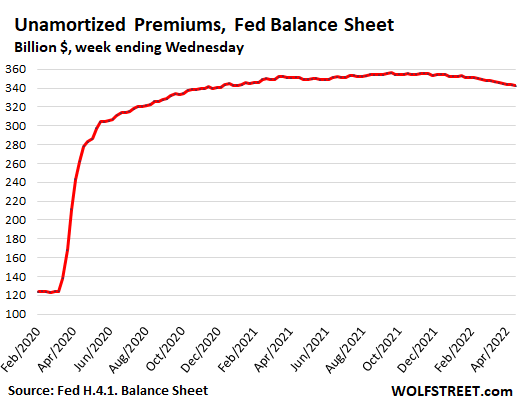

Unamortized premiums drop to $342 billion.

This is the net amount that the Fed paid in “premiums” over face value and paid in “discounts” below face value when buying Treasuries, MBS and US Treasury securities. agency in the market. The Fed books securities at face value and tracks the premium and discount separately.

Net unamortized premiums peaked in November 2021 at $356 billion and have now fallen to $342 billion:

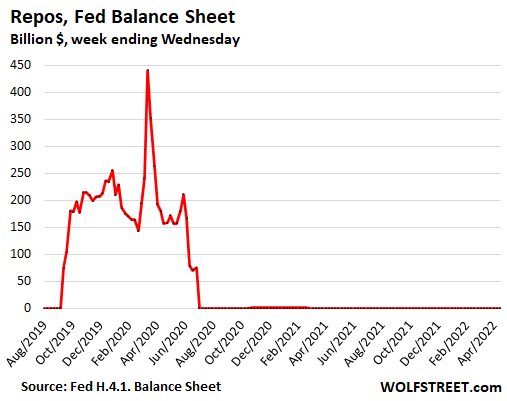

Repurchase agreements (Repos) at zero:

The Fed is still offering repos but has raised the rate it charges to be unattractive (currently 0.50%), and there have been no takers since July 2020 when the balance fell to zero .

With these repos, the Fed lends cash to counterparties on the repo market, in exchange for collateral (Treasury securities or MBS).

Repos are in-and-out transactions. On their due date – the next business day for overnight repos, or longer for forward repos – the Fed gets its money and the counterparty gets its security. Repos are a quick way for the Fed to send lots of cash into the markets and withdraw it when the repos mature.

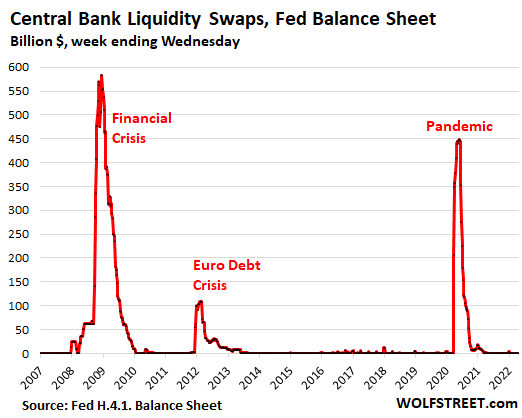

Central bank liquidity swaps are close to zero.

The Fed offered dollars to 14 other central banks through “central bank liquidity swaps,” in exchange for their currency, to provide dollars to those economies for their dollar funding needs. The Fed did this during the financial crisis in 2008-2010, during the euro debt crisis in 2011-2013 and during the pandemic.

Almost all of these swaps matured and were unwound, with the Fed getting its dollars back and other central banks getting the local currency back. Only a tiny $233 million worth of swaps remain outstanding:

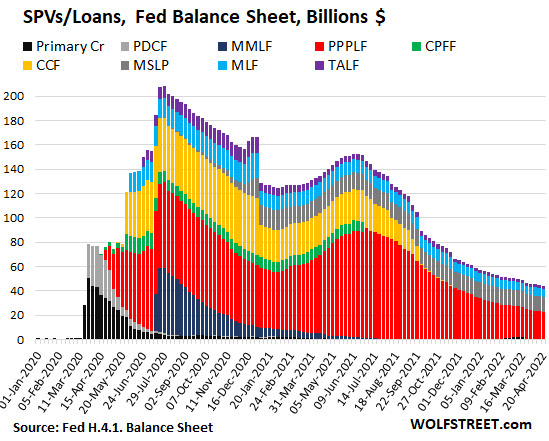

SPVs continue to decline.

Special Purpose Vehicles (SPVs) are legal entities (LLCs) that the Fed created during the crisis to purchase assets that it was otherwise not permitted to purchase. Equity financing was provided by the Treasury Department, which would bear the first loss on these assets. The Fed lends to SPVs and posts those loans and Treasury Department equity financing in those SPV accounts.

The total amount of SPVs fell 79% to $44 billion, from a peak of $208 billion in July 2020.

PPP loans the Fed purchased from banks account for $22 billion, or about half of total SPVs, up from $90 billion in July 2021. Over the summer and fall of 2021, the Fed has sold all of its corporate bonds and bond ETFs in the hottest corporate bond market ever, and they disappeared (yellow columns, CCF). The others are the Main Street Lending Program ($12 billion), the Municipal Liquidity Facility ($7 billion), and the TALF ($2 billion):

In addition to fueling the worst inflation in 40 years, the past two years of Fed QE and interest rate clampdowns have created the worst wealth disparity on record, based on the Fed’s own data. on the distribution of wealth in the United States. The ultimate result of the Fed’s reckless money printing is runaway inflation and this:

Do you like to read WOLF STREET and want to support it? You use ad blockers – I completely understand why – but you want to support the site? You can donate. I greatly appreciate it. Click on the mug of beer and iced tea to find out how:

Would you like to be notified by e-mail when WOLF STREET publishes a new article? Register here.

![]()