Growth cycle outlook: time is running out for risky assets

ijeab/iStock via Getty Images

For a few months now, I’ve been drumming about how economic growth is slowing and expected to deteriorate significantly in mid-2022. Unsurprisingly, my growth outlook hasn’t changed since I wrote my last article. detailing the subject.

Alas, we are increasingly approaching the inflection point where financial markets will succumb to the significant growth, liquidity and political headwinds that abound. In this Growth Cycle Outlook, I will repeat why I continue to believe that a significant deceleration in growth is likely to emerge over the next few quarters, and whether we will see a final rally in risk assets before that change. of trend.

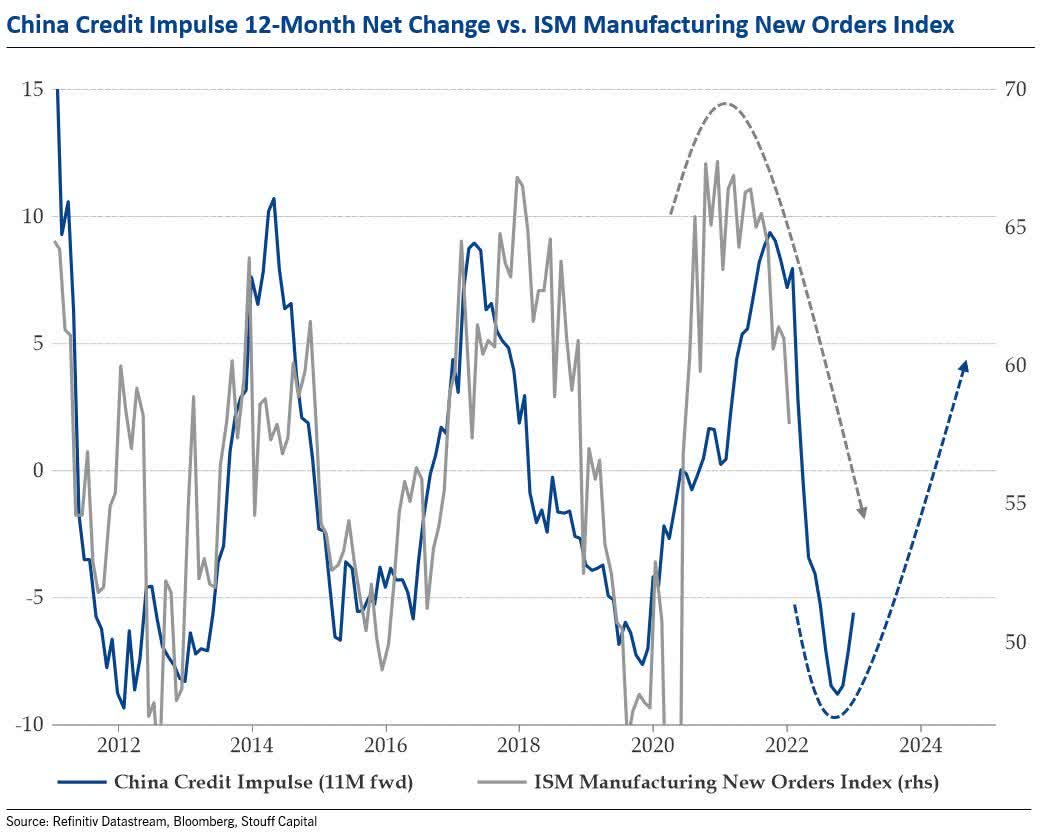

Checking the forward-looking leading indicators of economic growth, the Chinese credit impulse peaked in early to mid-2021 and its impact is clearly starting to be felt in developed markets.

Source: Julien Bitel

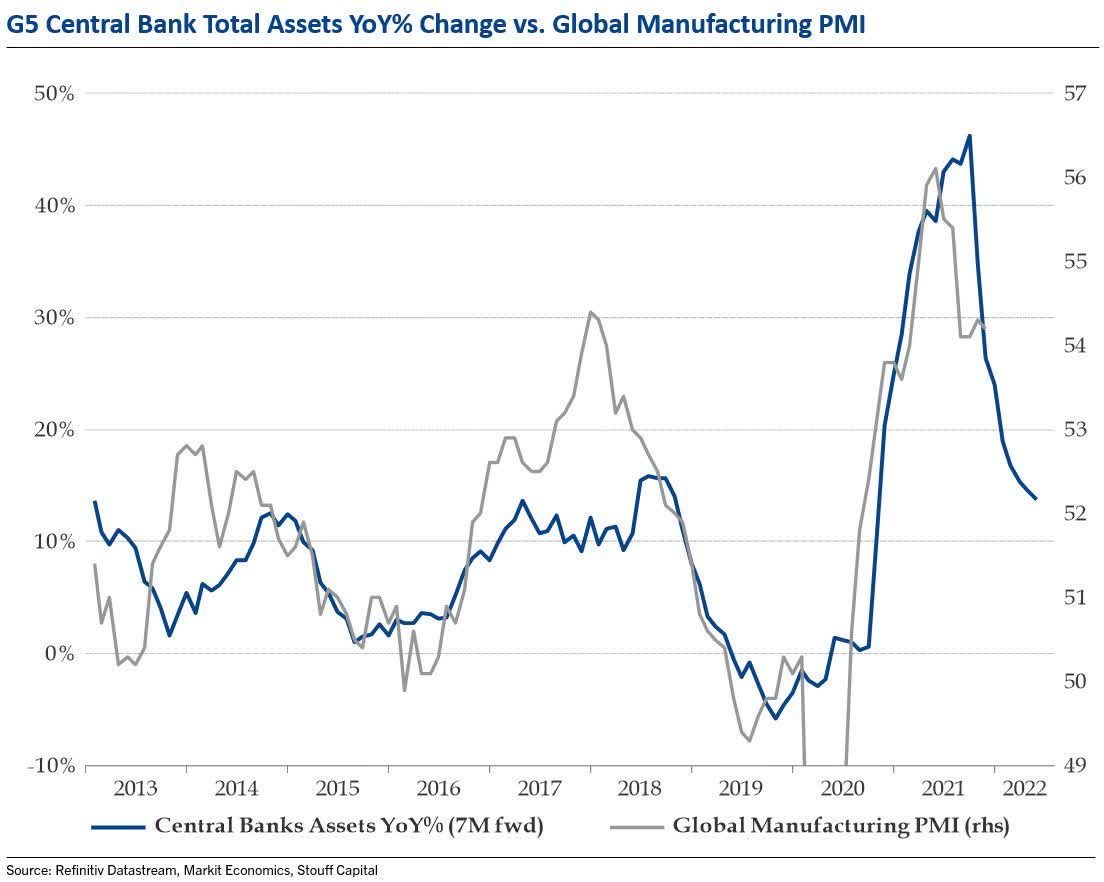

Asset purchases by G5 central banks also signal that global PMIs are likely to decline over the coming quarters.

Source: Julien Bitel

While the weekly leading index from the Business Cycle Research Institute (ECRI) continues to decline from its peak nearly 12 months ago.

Source: Lakshman Achuthan

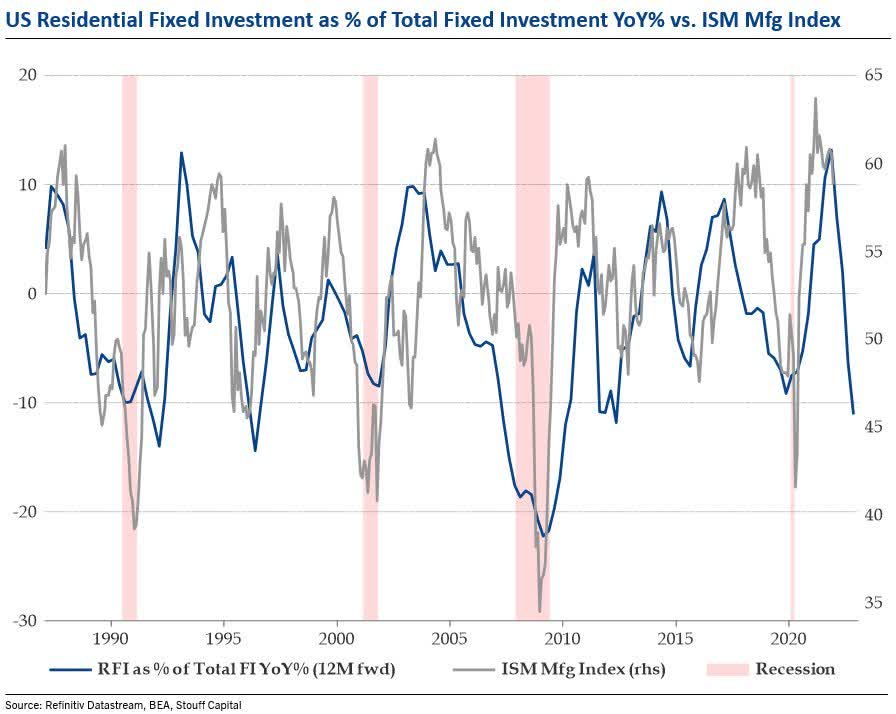

The housing market is only confirming this message, pointing to an ISM below 50 in the coming months.

Source: Julien Bitel

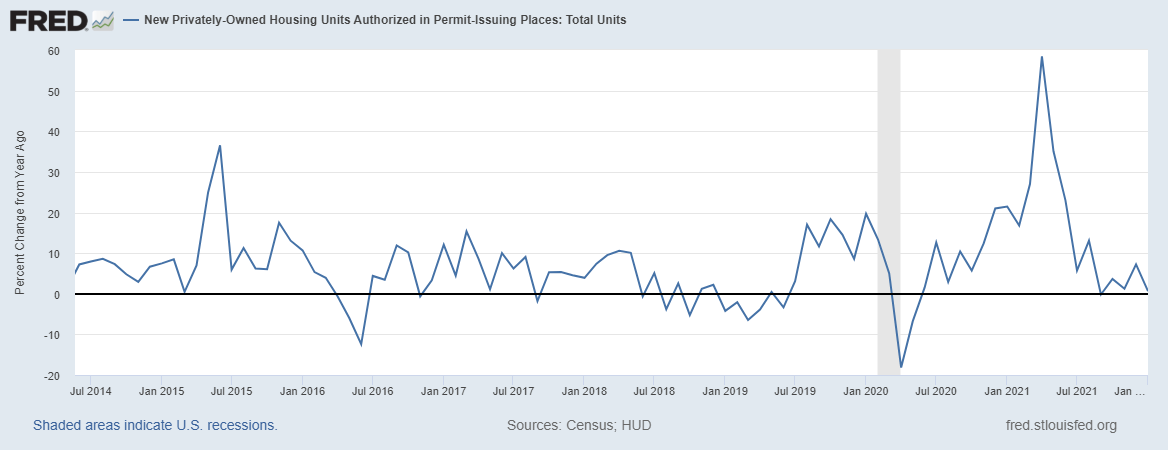

The deceleration in fixed residential investment is accompanied by building permits, which are flirting with near-negative year-on-year growth.

St. Louis Fred

Given the importance of the housing sector to the economy, the implications for economic growth are clear and obvious.

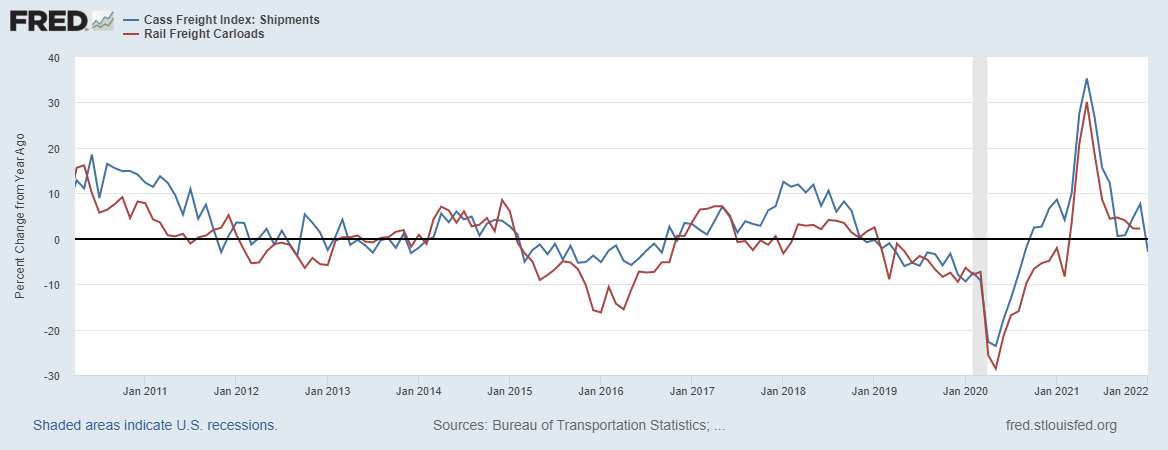

In terms of consumption and demand, carloads and freight shipments look very weak.

St. Louis Fred

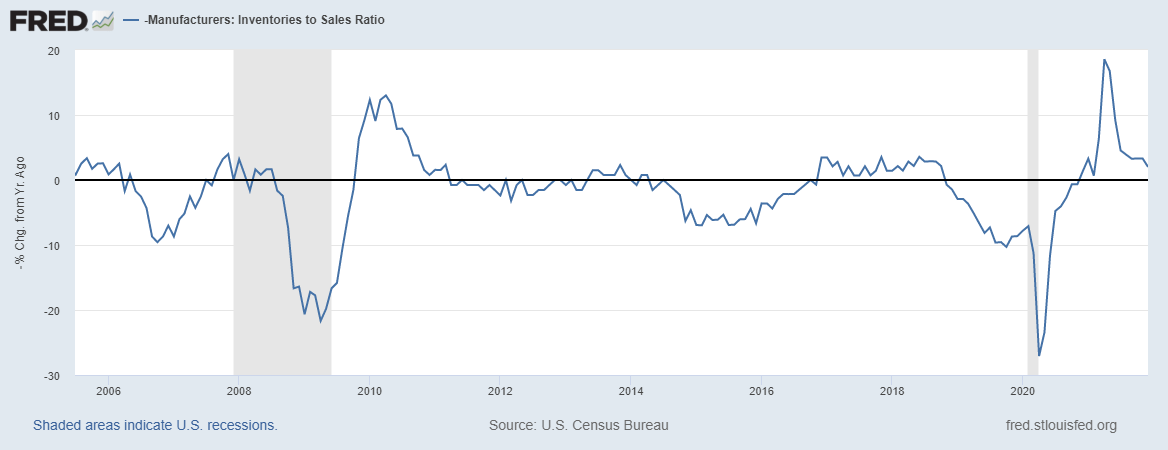

While the manufacturing sales to inventory ratio continues to decline (reversed below). When sales increase at a faster rate than inventory and the ratio increases, more inventory must be produced, which puts upward pressure on prices as well as an increased need for workers and hours worked, therefore positive for growth. When inventory increases faster than sales and the ratio decreases, the reverse occurs. Clearly, demand continues to falter.

St. Louis Fred

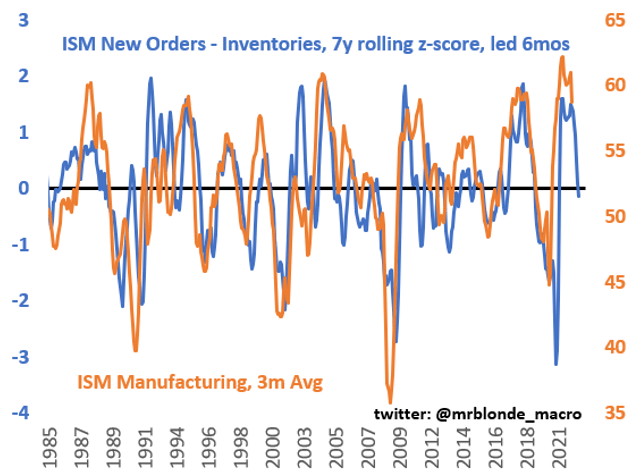

If we get this ratio from the ISM manufacturing survey via the gap between new orders and inventories, the message is the same…

Source: Mister Blonde Macro

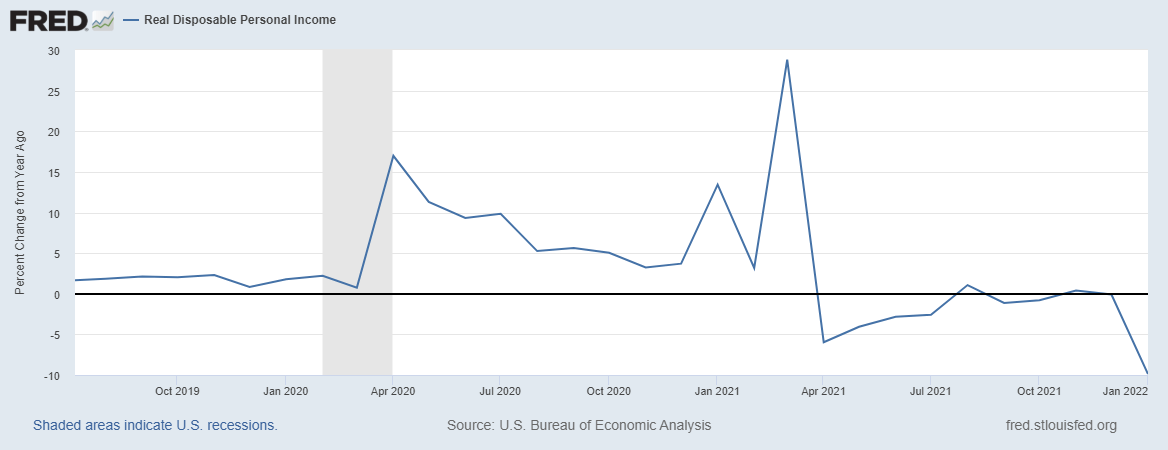

Obviously, demand is falling and the economy is slowing down. Inflation has completely wiped out real income growth.

St. Louis Fred

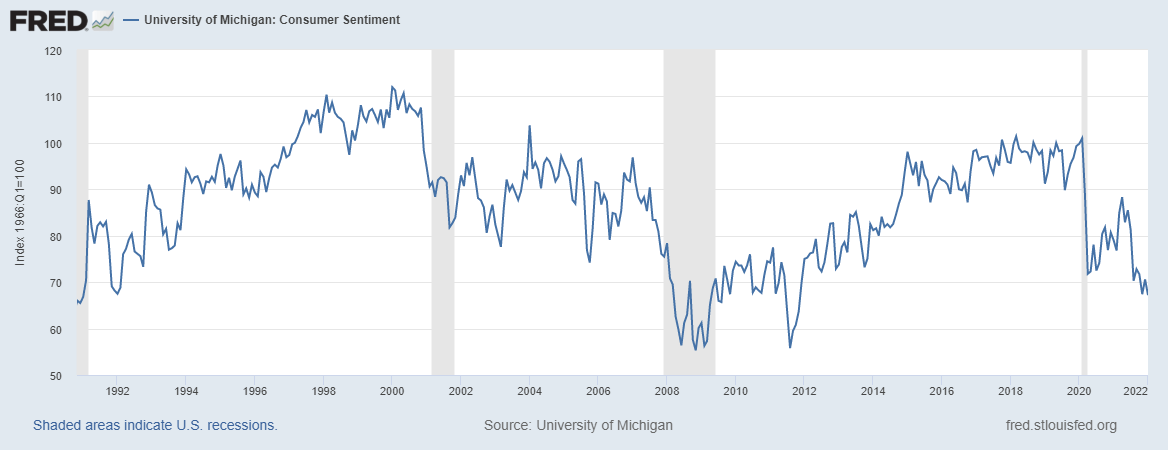

As a result, not only is consumer sentiment below what it was at the start of the pandemic, it is now at its lowest level in a decade.

St. Louis Fred

Add to that every 50% rise in oil prices in the past has preceded a recession…

It’s not hard to see how inflation destroys incomes, demand and consumer confidence. We are clearly in the latter stages of the economic cycle.

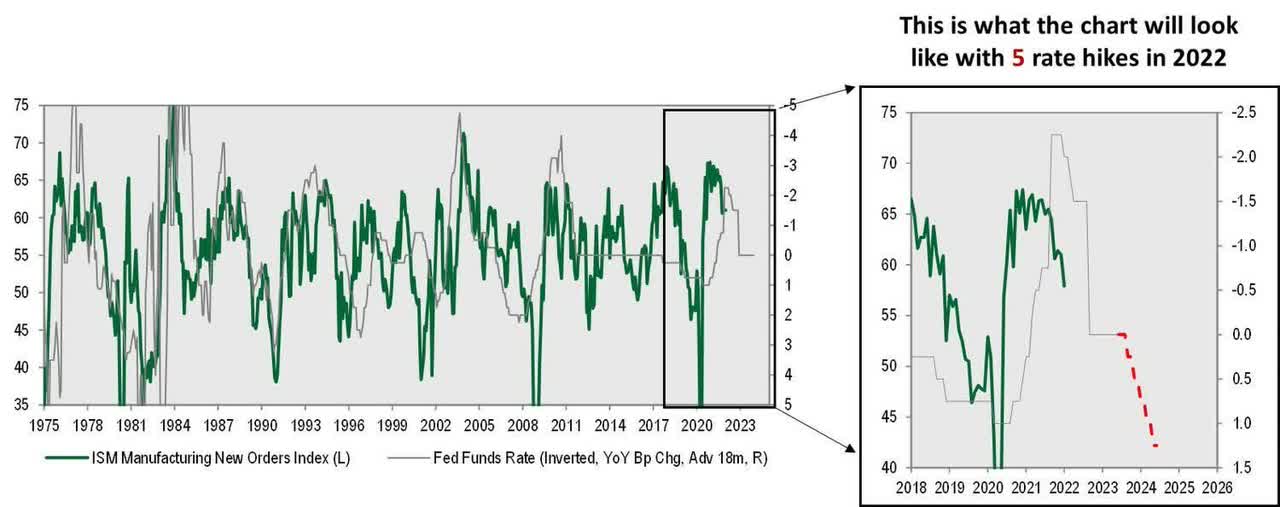

So what is the solution ? Tighten financial conditions in an economic downturn by increasing borrowing costs…

Source: Michael Kantrowitz, CFA

As we can see above, such actions will clearly reinforce the downturn. The Fed, of course, has no choice in the matter because it is part of its mandate to achieve stable prices, and all it can do is use the tools at its disposal to try to achieve it. It turns out that the tools at his disposal have no ability to affect inflation. Such is the damage of inflation on the economy.

For risky assets, what matters to a large extent for their performance is the direction of the rate of change of growth, as well as inflation. As I have explained so far, growth is slowing and is expected to slow noticeably throughout 2022.

More concerning is that inflation is also expected to ease on a rate of change basis in the second half of 2022 (I have discussed this dynamic and its implications in detail here). If growth and inflation did indeed slow in parallel over the course of the year, then we get a clear signal to be cautious about pro-cyclical risk assets during those times. Add to this momentum a tightening of monetary policy and a fiscal situation that has shifted from fiscal stimulus to fiscal slowdown, investors would do well to position themselves appropriately for the year ahead.

It is exactly the opposite dynamics that have driven markets higher throughout the second half of 2020 and into 2021, a period in which we have had an acceleration in growth and inflation, record quantitative easing , fiscal stimulus and excess liquidity. Expect markets to behave accordingly as these factors now reverse on the downside.

For a more detailed discussion of the short and long leading indicators of economic growth and their implications going forward, please see my earlier thoughts on the outlook for the January and December growth cycle.

Now, having said all of that, the question then becomes, when will this slowing growth environment actually show up in asset markets. It is important to remember when discussing the macro and business cycle forecast that you are trying to live in the future. The macro is slow and quite difficult to time to perfection. So, despite the recent weakness in equities, could we see one last mid-year rally before we see the real growth deceleration? That seems like a distinct possibility.

Indeed, there are a number of signs suggesting that the bottom could be reached for stocks at the moment.

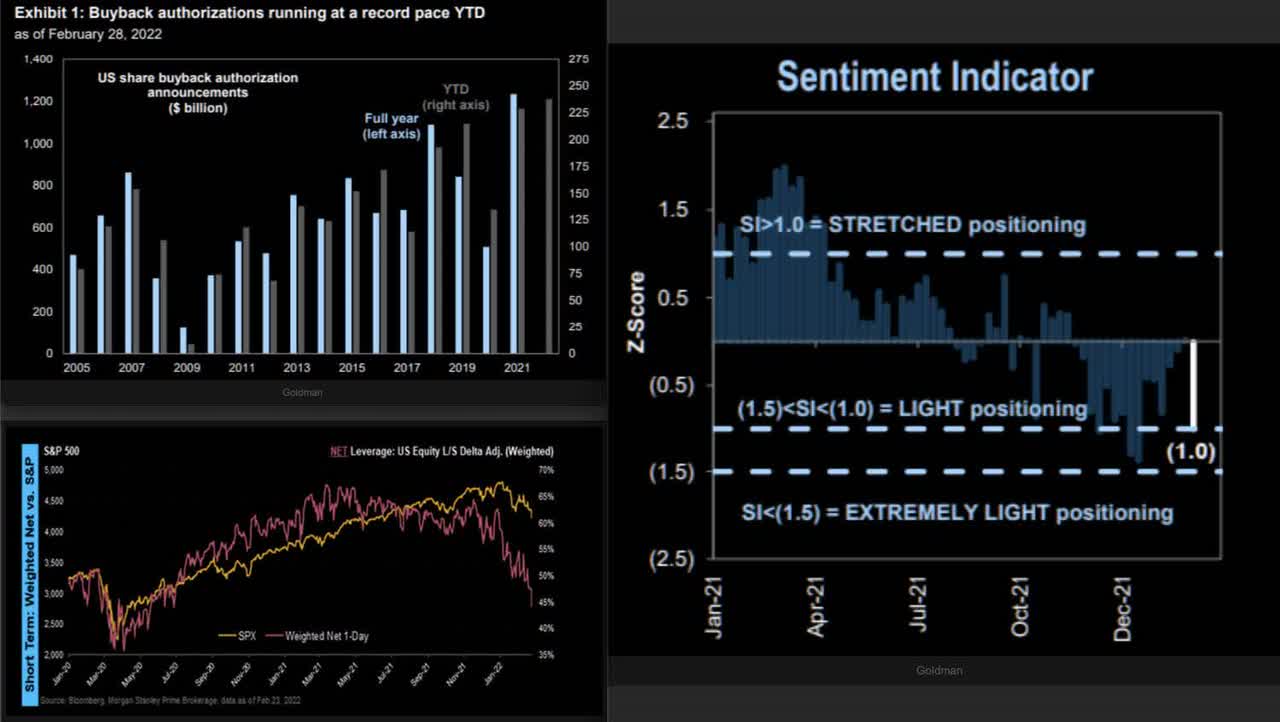

First, as shown below, we can see that corporate takeover clearances are unfolding at a record pace since the start of the year, while sentiment has reached extreme levels of fear. Speculative leverage has also declined significantly over the past two months.

Source: Imran Lakha – Options Overview

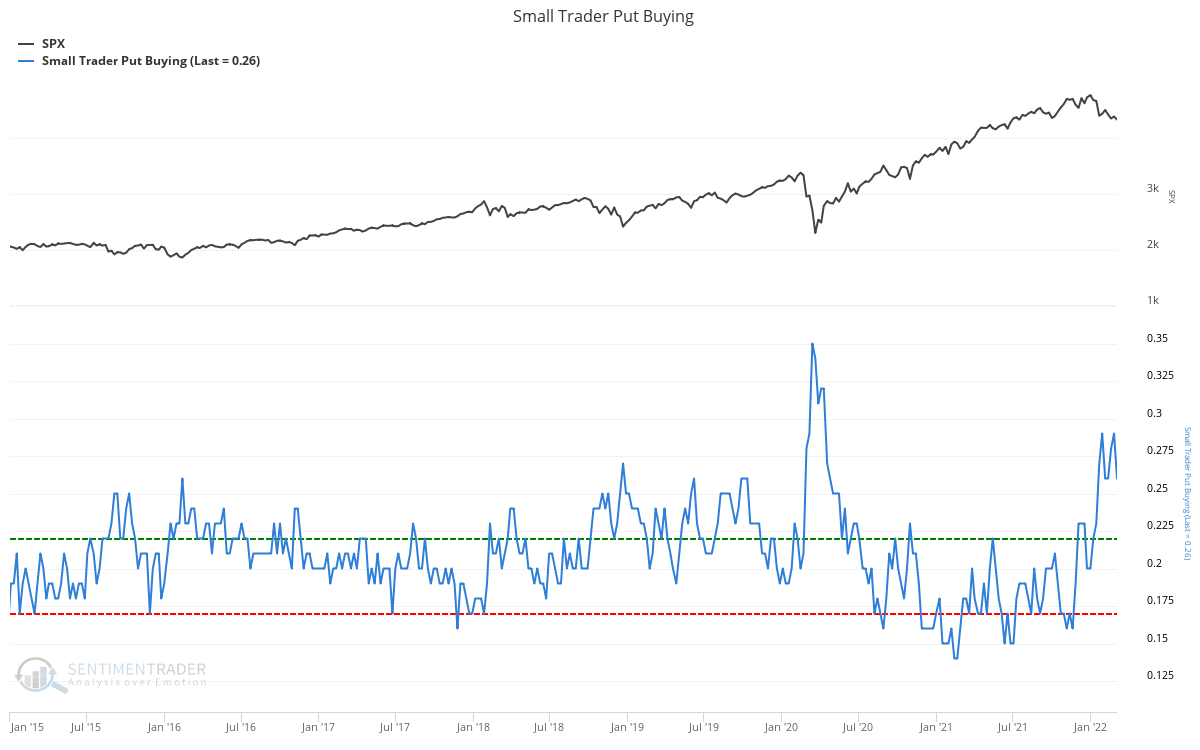

Investors piled into hedges via put options, again indicative of extreme fear.

Sentiment Trader

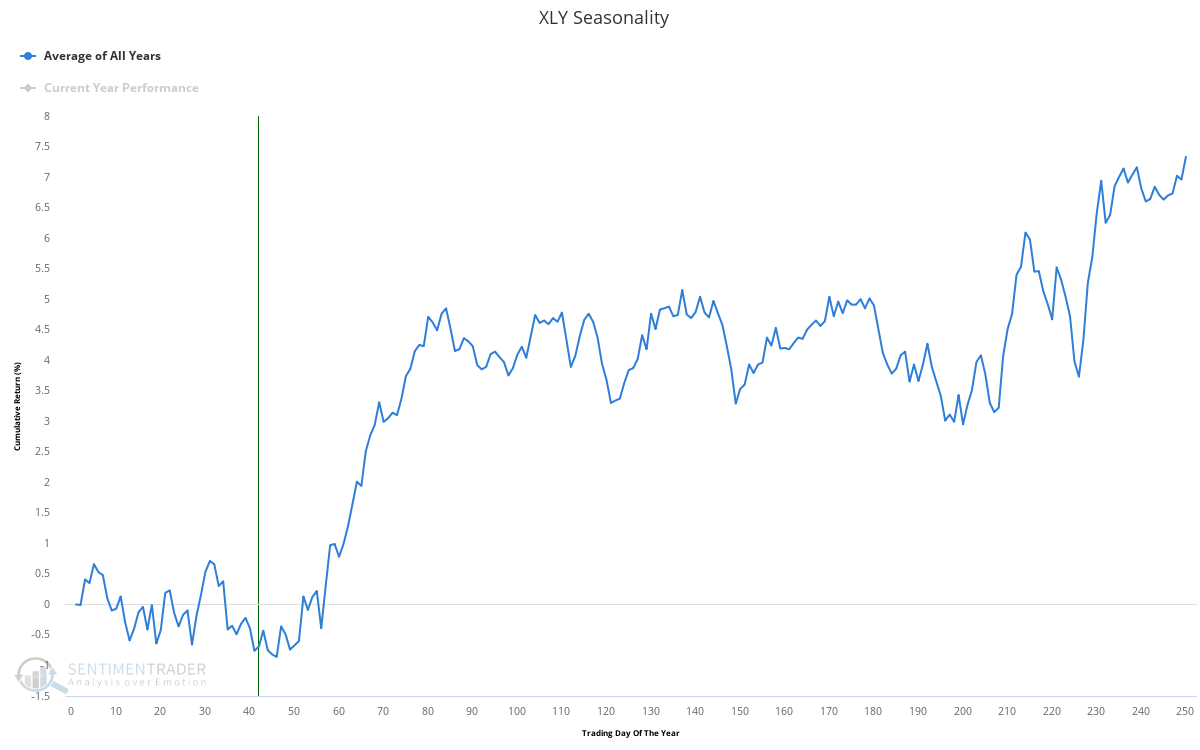

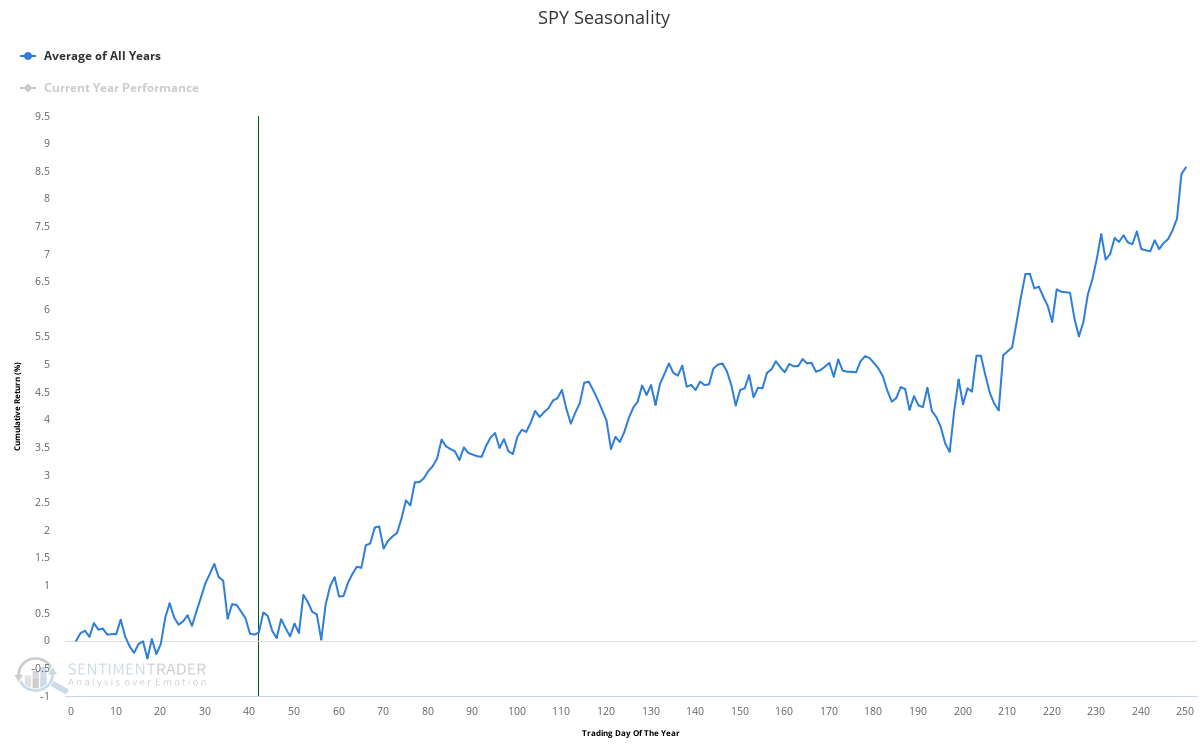

Meanwhile, the seasonality of discretionary stocks and most pro-cyclical stocks is poised to enter the most favorable months of the year in March and April.

Sentiment Trader

As is the stock market as a whole (and yes, due to the seasonality of the market structure Is question).

Sentiment Trader

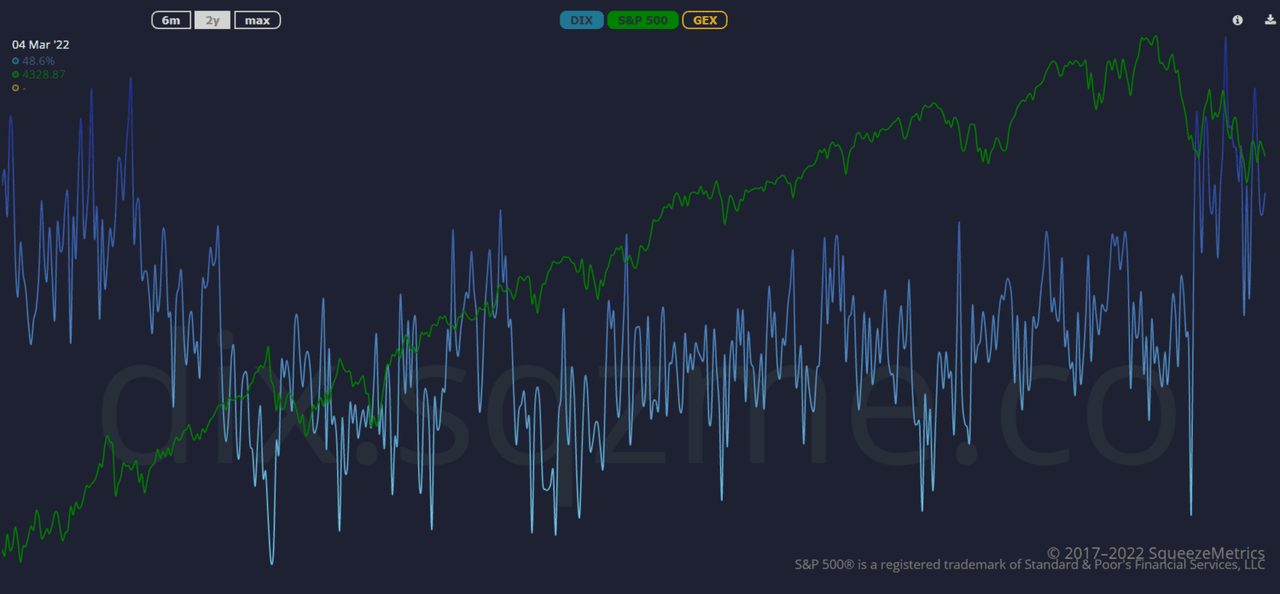

And finally, dark pools have been seeing a significant level of bullish activity lately, suggestive of positive market returns over the next one to two months.

Source: Compression Metrics

As we can see, although we are in the midst of a downturn in the growth cycle, there is reason to believe that we could see a rally in equity markets over the next two to three months. However, given the lackluster macro backdrop, there are no guarantees and investors should be strong sellers and seize such an outcome as an opportunity to raise cash and position portfolios more defensively.

Summary and key takeaways

-

Leading indicators of economic growth point to a significant slowdown as 2022 progresses. This is not a favorable environment for pro-cyclical stocks and risky assets.

-

The Fed is in a difficult position where it has no choice but to tighten monetary conditions in the event of an economic slowdown. Given that lagging strong economic data (via a tight labor market and low levels of unemployment) continues to point to a robust economy, coupled with persistent inflation, this will likely keep the Fed on its tightening path in a foreseeable future. The Fed put will likely be hit lower than what we have seen in the past.

-

Moreover, better economic data releases are not necessarily bullish for equities, as it keeps the pressure on the Fed for more aggressive tightening, even with high inflation readings in the coming months.

-

If we see a mid-year rally in equity markets in the face of a severe slowdown in growth, now would seem a good time to take profits and position portfolios more defensively.

-

Investors would do well to focus on capital preservation rather than capital appreciation over the coming year. A growth slowdown is no time to be a business hero.

Editor’s note: The summary bullet points for this article were chosen by the Seeking Alpha editors.