/cloudfront-us-east-2.images.arcpublishing.com/reuters/ADFMQ2FDGNNFRJ2Z3G5RJLM7VE.jpg)

Join now for FREE unlimited access to Reuters.com

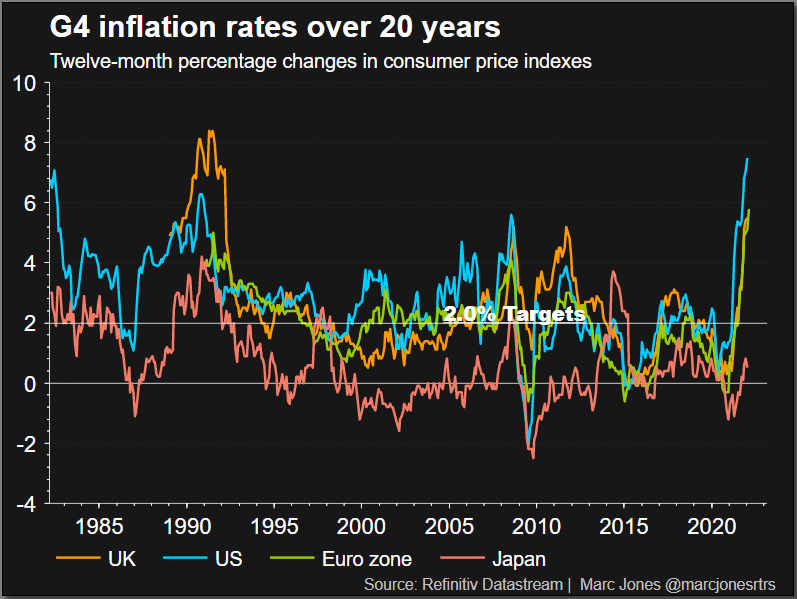

LONDON, March 4 (Reuters) – Terminal inflation rates more than terminal interest rates could be a better guide to how global currencies are riding the post-pandemic world and the commodity shock caused by the war.

As major central banks prepare to normalize very loose monetary policies and near-zero interest rates in the face of soaring oil and food prices – driven by the reopening of economies and spurred by the invasion of Ukraine by Russia – there’s a lot of concern about how high interest rates will have to go.

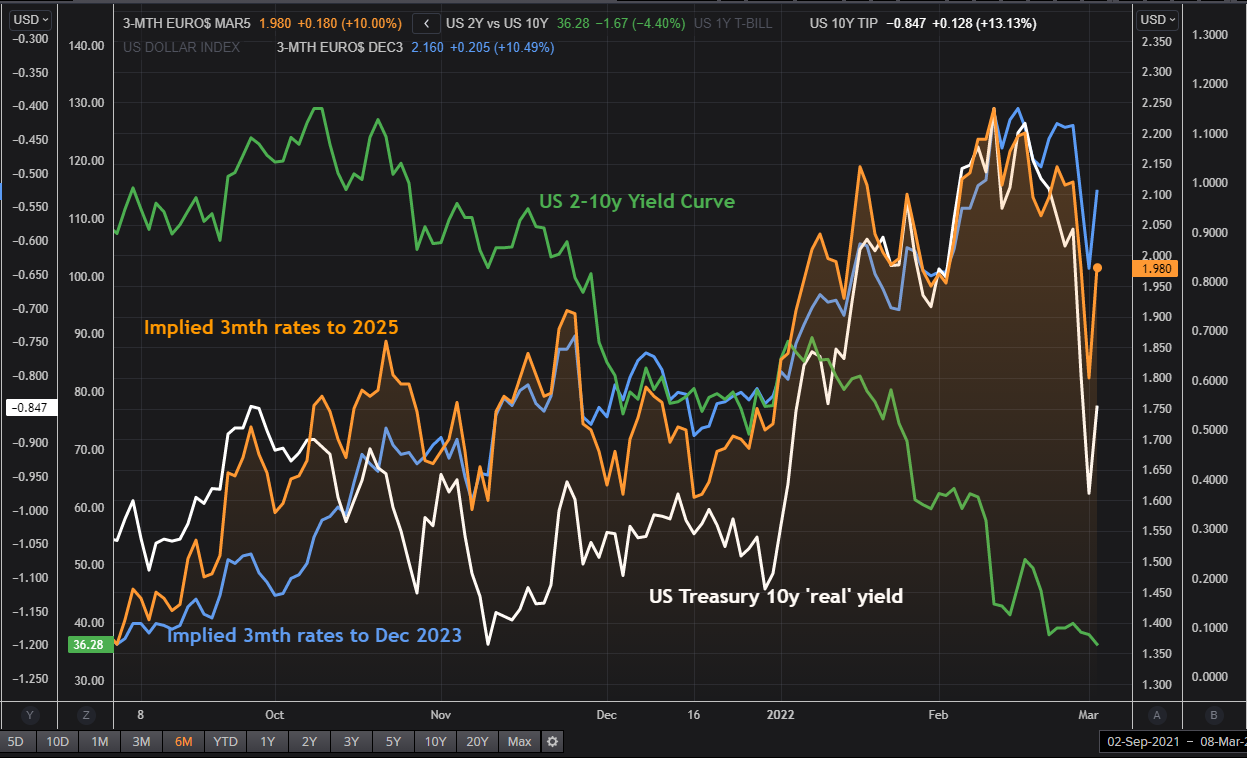

Markets speak of “terminal” interest rates as the high point of the coming cycle. Even if the US Federal Reserve, for example, points to a “neutral” rate between 2 and 2.5%, and its determination to go higher if necessary, the futures markets are still in doubt and see rates capping the year next around 2% or less. Read more

Obtaining this horizon is essential for borrowers who need to plan ahead and for future stock and bond market prices.

But for currencies, it is long-term inflation differentials that should generally determine value over time.

And so where markets assume inflation rates end – which itself is a function of their confidence in each central bank’s willingness or ability to bring price increases back to target – is as important than relative terminal interest rates.

And in some respects that maximum interest rate will reflect what a central bank is willing to tolerate on the inflation front, especially if there is a clearer trade-off between ever-tighter policy and growth or poverty. employment during this period.

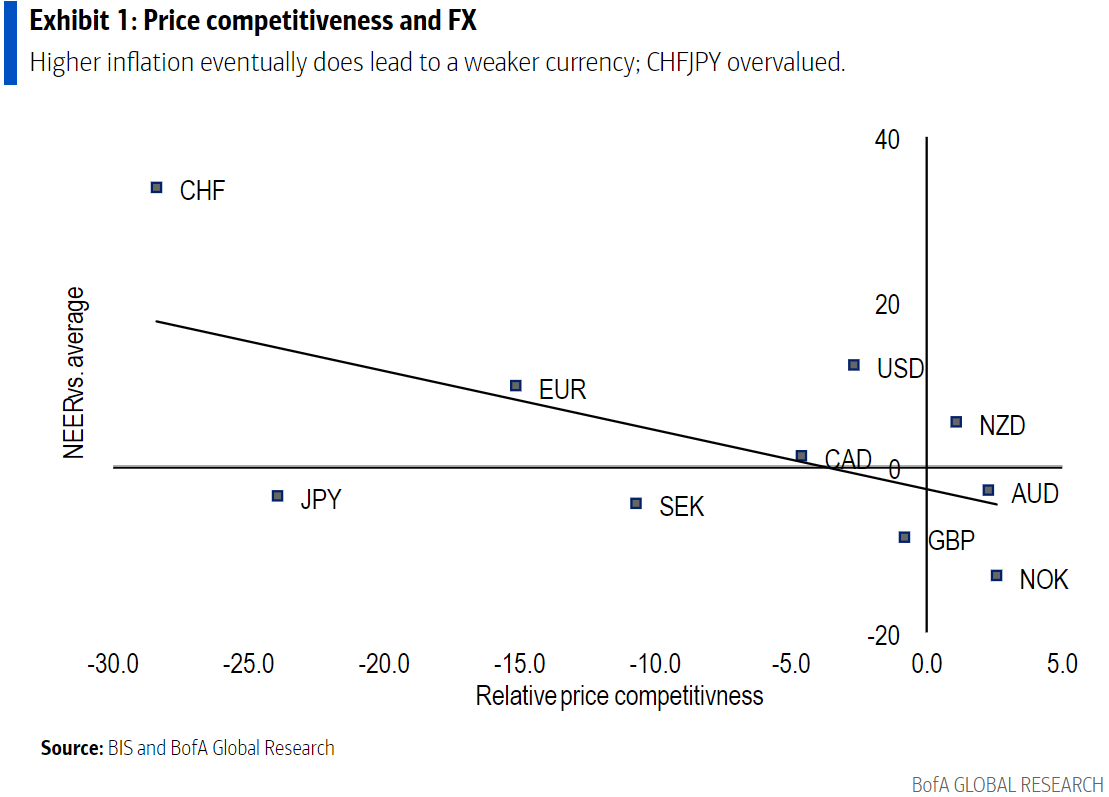

In a report released last week, Bank of America’s Athanasios Vamvakidis sketched out this arcuate path of a higher US dollar today that is rapidly receding as US inflation momentum erodes it over time. time compared to Japan, the euro zone and Switzerland.

More aggressive Fed tightening this year is now supporting the dollar against the euro. But if US inflation is likely to settle above 2% in the long term – as BofA predicts – and Europe and Japan fall back below, this corresponds to a return of the euro/dollar exchange. as high as $1.20 by 2024.

“Much hinges on the credibility of the central bank,” Vamvakidis wrote, arguing that faith in central banks’ inflation-fighting pedigree means that higher inflation rates today lead to lower inflation rates. higher interest and stimulate the currency.

But beyond the short term? “With inflation currently above target in most G10 countries, the currency implications also depend on where countries end up.”

“Countries with sustainably higher inflation will also end up with weaker currencies,” Vamvakidis wrote. the correlation goes both ways.

MONEY AND INFLATION

Of course, there are myriad influences on short-term exchange rates – relative growth and interest rates, high-frequency economic polls, fiscal policies, changing sentiment about geopolitics or elections, and the ebb and flow of speculative, investment or commercial flows.

But just as inflation dictates the value of the dollar or euro in your pocket – by measuring the amount of bread, milk and goods and services you can buy with it from year to year – it also affects the relative competitiveness of an economy and its companies abroad – and therefore its exchange rate.

In other words, if higher inflation weakens the purchasing power of a currency domestically, relatively higher inflation, along with rising wages and input costs, weakens that currency externally. , as exchange rates evolve to compensate for the loss of competitiveness. Or so the theory goes.

The problem goes to the heart of the “carry trade” anomaly, where traders seek out short-term bets by borrowing currencies with low funding rates and depositing them in a higher-yielding currency – pocketing the spread as long as the exchange rate does not rotate.

As these are generally short-term bets, little attention is paid to the real reason why rates are higher in the former – and this is often due to a chronic inflation problem.

As carry trades typically operate in times of low volatility, we may be at some point. Global foreign exchange markets have just gone through a period of extraordinarily low volatility for major currencies – in part due to years in which inflation rates and inflation expectations in the world’s largest economies had all converged in below 2% targets.

This world may be ending.

The CVIX Index (.DBCVIX) of major currency implied volatility hit an all-time high on the eve of the pandemic – but has since doubled. Despite everything, the three-month implied flight of the euro/dollar remains below its 30-year average.

If inflation differentials trump carry in more volatile work, what to watch?

As uncertain and frantic as the current economic and political circumstances are, market assumptions about long-term inflation and “real” inflation-adjusted spreads are in sight.

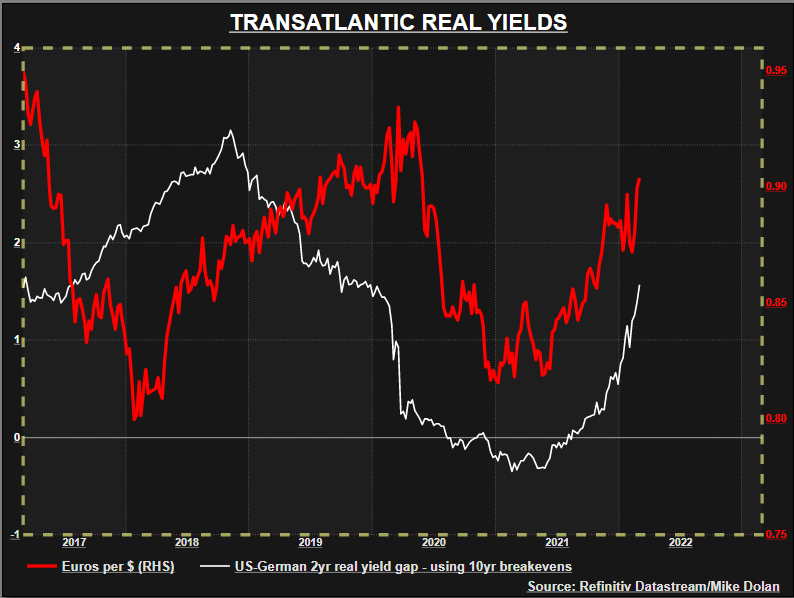

On this point, US 10-year inflation expectations at over 2.7% are more than half a percentage point higher than euro equivalents, even if the Fed acts earlier than the European Central Bank to raise rates. But the price of oil on Ukraine has also seen the latter jump above 2%.

A tough-talking Fed is gaining momentum in currencies today as the Dollar soars. But he may have to match words with actions over the coming year to keep him here.

The author is Finance and Markets Editor at Reuters News. All opinions expressed here are his own.

by Mike Dolan, Twitter: @reutersMikeD Editing by Alexandra Hudson

Our standards: The Thomson Reuters Trust Principles.

The opinions expressed are those of the author. They do not reflect the views of Reuters News, which is committed to integrity, independence and non-partisanship by principles of trust.